Introduction

For many people, purchasing a home is one of the biggest financial decisions they will ever make. Since buying a property often requires a substantial amount of money, many homebuyers rely on mortgage loans to finance their purchase.

A mortgage loan allows borrowers to purchase a home while repaying the borrowed amount over time through scheduled monthly payments. Understanding how mortgage loans work can help prospective homeowners make informed decisions and choose financing options that align with their financial goals.

This guide explains mortgage loans, how they work, their benefits, eligibility requirements, application process, and important considerations for borrowers.

What Is a Mortgage Loan?

A mortgage loan is a type of secured loan used to purchase residential property. The property itself serves as collateral for the loan, meaning the lender has a legal interest in the property until the loan is fully repaid.

Mortgage loans typically include both principal and interest payments and may also include property taxes, homeowners insurance, and other applicable costs depending on the loan agreement.

Mortgage terms can vary based on the lender, loan type, and borrower qualifications.

How Mortgage Loans Work

Mortgage loans follow a structured borrowing and repayment process.

Application

Borrowers submit financial information and property details to a lender for review.

Approval Process

Lenders evaluate credit history, income, employment status, debt obligations, and other financial factors.

Property Valuation

A property appraisal may be conducted to determine the home’s market value.

Loan Approval

Once requirements are satisfied, the lender issues loan approval and financing terms.

Home Purchase

Loan funds are used to complete the property purchase.

Repayment

Borrowers make regular monthly payments until the loan balance is paid in full.

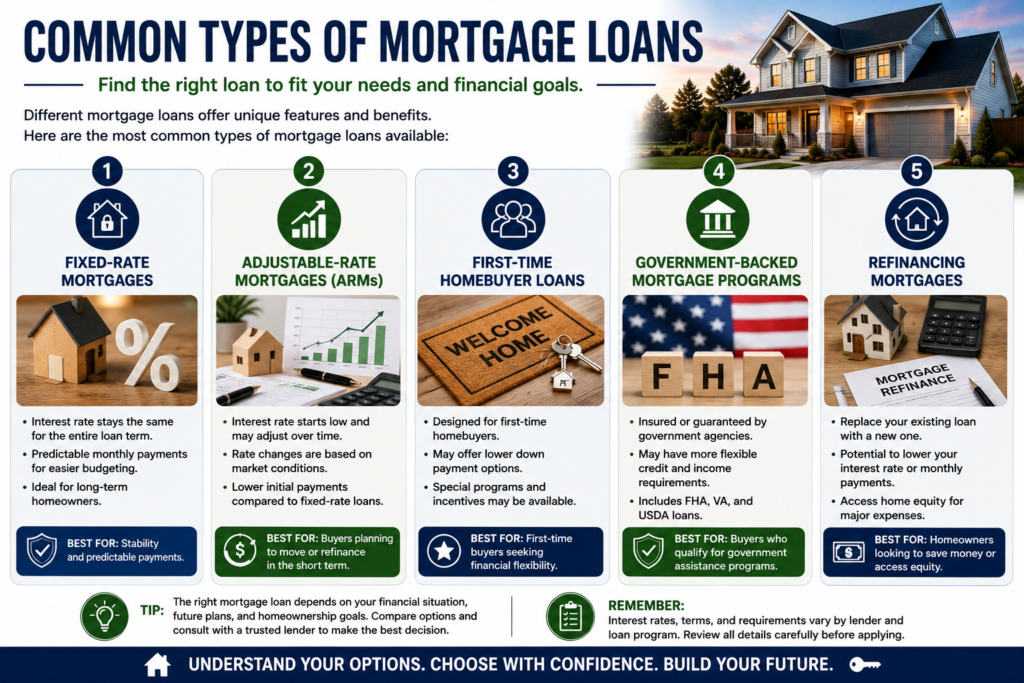

Common Types of Mortgage Loans

Fixed-Rate Mortgages

Interest rates remain unchanged throughout the loan term, providing predictable monthly payments.

Adjustable-Rate Mortgages (ARMs)

Interest rates may change periodically based on market conditions.

First-Time Homebuyer Mortgages

Special programs may be available for eligible first-time homebuyers.

Government-Backed Mortgage Programs

Some mortgage programs are supported by government housing initiatives.

Refinancing Mortgages

Refinancing allows homeowners to replace an existing mortgage with a new loan under different terms.

Benefits of Mortgage Loans

Homeownership Opportunities

Mortgage financing makes homeownership accessible for many individuals and families.

Spread Costs Over Time

Borrowers can repay the home purchase over an extended period.

Potential Property Appreciation

Real estate may increase in value over time.

Build Home Equity

Each mortgage payment may increase ownership equity in the property.

Financial Stability

Fixed payment structures can support long-term financial planning.

Eligibility Requirements

Mortgage loan requirements vary by lender but commonly include:

Credit History

Lenders review creditworthiness and repayment history.

Income Verification

Applicants generally need proof of stable income.

Employment History

Consistent employment may strengthen an application.

Down Payment

Many mortgage programs require a down payment.

Debt-to-Income Ratio

Existing financial obligations are considered during approval.

Property Requirements

The property must usually meet lender standards and valuation requirements.

Documents Commonly Required

Applicants may need to provide:

- Government-issued identification

- Proof of income

- Employment verification

- Bank statements

- Tax returns

- Credit information

- Property purchase agreement

- Property appraisal documents

- Down payment verification

Requirements vary depending on the lender and loan program.

How to Apply for a Mortgage Loan

Review Your Financial Situation

Evaluate your income, expenses, savings, and credit profile.

Determine Your Budget

Estimate how much home you can comfortably afford.

Compare Mortgage Options

Research available loan programs and lenders.

Gather Documentation

Prepare required financial and property-related documents.

Submit an Application

Complete the lender’s mortgage application process.

Complete Closing Requirements

Review final loan documents and complete the property purchase transaction.

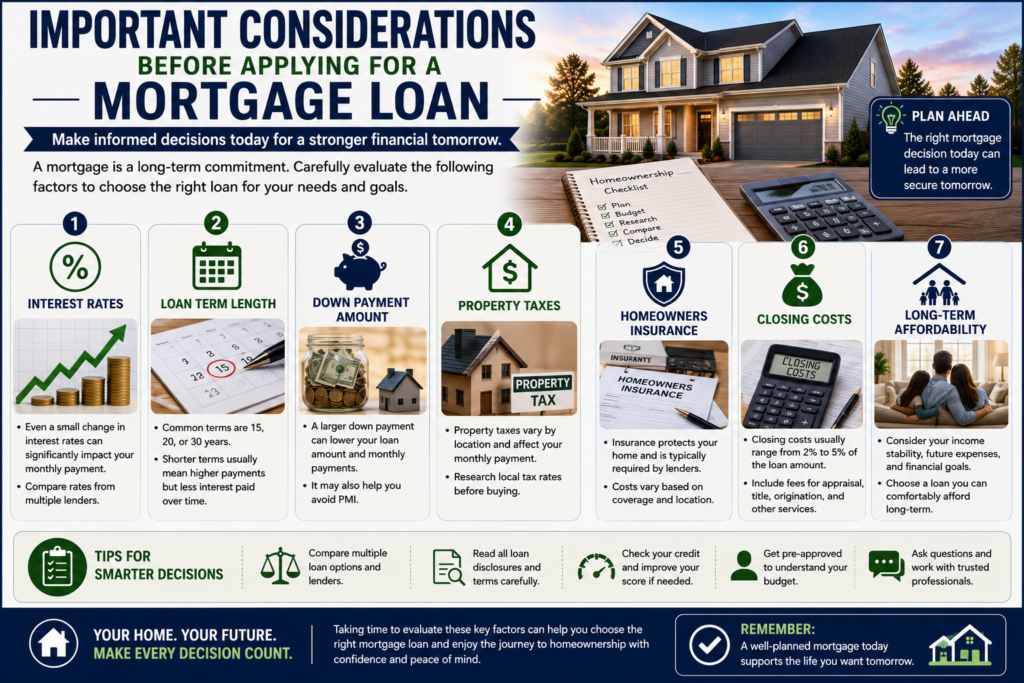

Important Considerations

Interest Rates

Mortgage rates significantly affect overall borrowing costs.

Loan Term Length

Shorter terms may reduce total interest but increase monthly payments.

Down Payment Amount

Larger down payments may reduce loan balances and borrowing costs.

Property Taxes and Insurance

These expenses may be included in monthly mortgage payments.

Closing Costs

Additional fees may apply during the home purchase process.

Long-Term Affordability

Borrowers should ensure mortgage payments fit comfortably within their budget.

Frequently Asked Questions

What is a mortgage loan?

A mortgage loan is financing used to purchase a home or residential property while repaying the borrowed amount over time.

How long do mortgage loans last?

Loan terms vary, but common mortgage terms may range from several years to multiple decades.

Is a down payment required?

Many mortgage programs require a down payment, although requirements vary.

Can I refinance my mortgage?

Yes. Refinancing may allow homeowners to replace an existing mortgage with a new loan.

What affects mortgage approval?

Factors often include credit history, income, employment, debt levels, and property valuation.

Conclusion

Mortgage loans play an essential role in helping individuals and families achieve homeownership. By understanding how mortgage loans work, comparing available options, and carefully reviewing financial obligations, borrowers can make informed decisions that support their long-term housing and financial goals.

Before applying, take time to evaluate your budget, research lenders, and understand the full cost of homeownership to ensure that a mortgage loan aligns with your needs and future plans.