Personal Loan Guide: Everything You Need to Know Before Applying

Introduction

Personal loans have become one of the most popular financing options for individuals who need access to funds for various purposes, including debt consolidation, home improvements, medical expenses, education costs, and unexpected emergencies. Unlike secured loans, most personal loans do not require collateral, making them accessible to a wide range of borrowers.

Understanding how personal loans work is essential before submitting an application. Borrowers should evaluate interest rates, repayment terms, eligibility requirements, and their own financial situation to ensure they make informed decisions.

This guide covers everything you need to know about personal loans, including their benefits, potential drawbacks, application process, and tips for improving approval chances.

What Is a Personal Loan?

A personal loan is a type of installment loan that allows borrowers to receive a lump sum of money and repay it through fixed monthly payments over an agreed period.

Personal loans can be used for various legitimate purposes, including:

- Debt consolidation

- Medical expenses

- Home improvements

- Wedding expenses

- Emergency situations

- Education-related costs

- Major purchases

Most personal loans come with fixed interest rates and predictable monthly payments, making budgeting easier for borrowers.

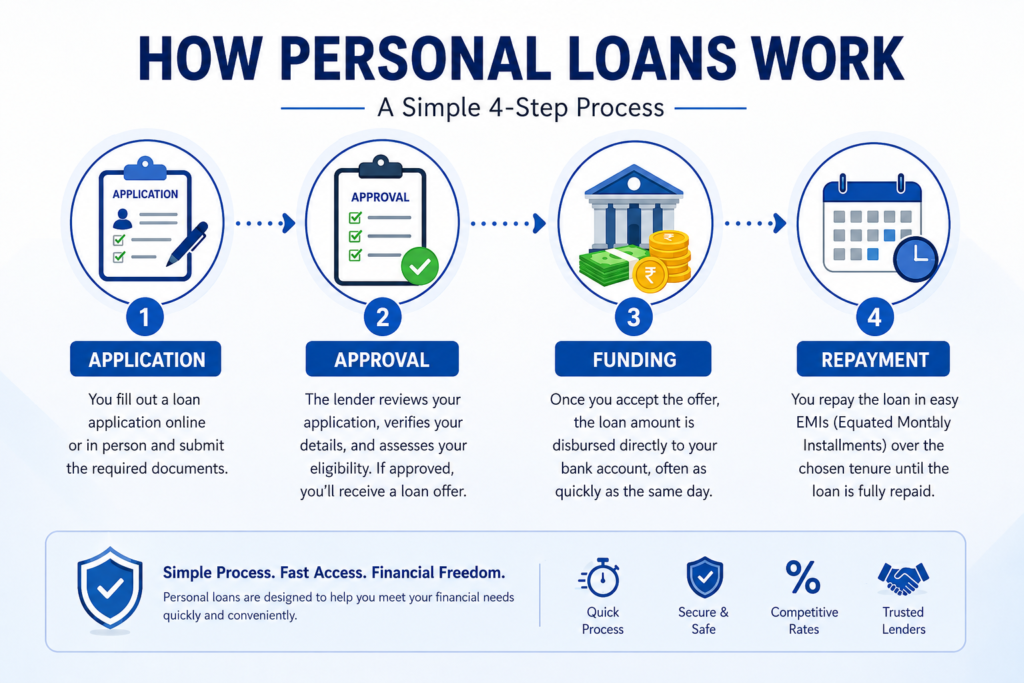

How Personal Loans Work

When a borrower applies for a personal loan, lenders evaluate several factors, including income, employment status, credit history, and existing financial obligations.

If approved, the borrower receives the loan amount and agrees to repay it according to the loan terms. Payments typically include both principal and interest.

The key components of a personal loan include:

Loan Amount

The total amount borrowed from the lender.

Interest Rate

The percentage charged by the lender for borrowing money.

Loan Term

The repayment period, which may range from several months to several years.

Monthly Payment

The fixed amount paid each month until the loan is fully repaid.

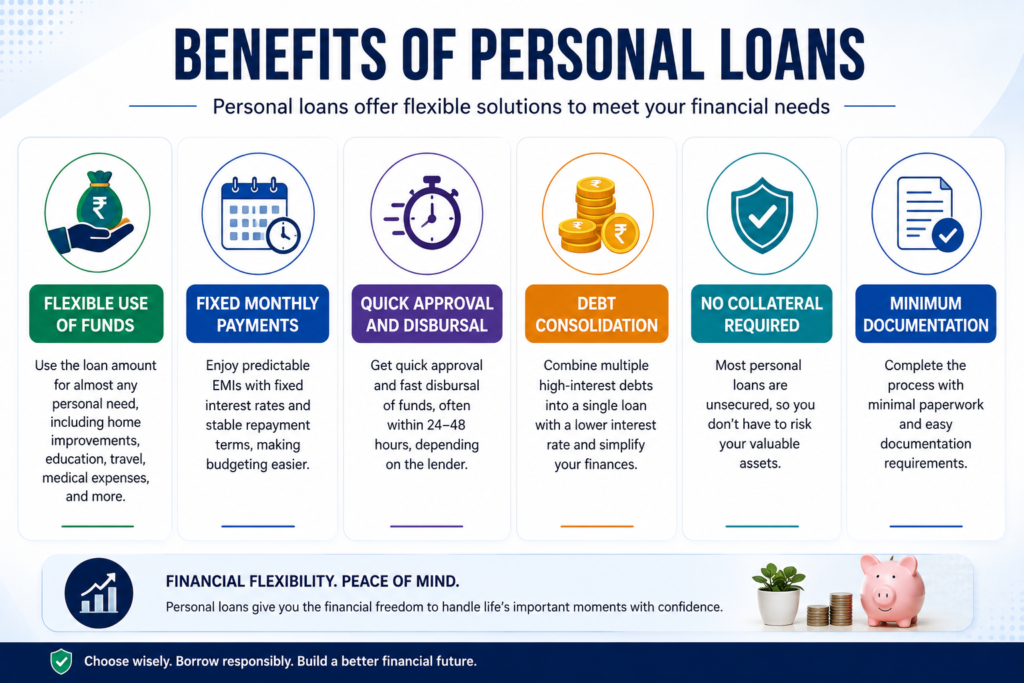

Benefits of Personal Loans

Flexible Use of Funds

Personal loans can be used for a wide variety of personal financial needs.

Fixed Monthly Payments

Many personal loans offer predictable repayment schedules.

Faster Access to Funds

Qualified borrowers may receive funding quickly after approval.

Debt Consolidation Opportunities

Combining multiple debts into one loan can simplify financial management.

No Collateral Required

Many personal loans are unsecured, reducing risk to personal assets.

Potential Drawbacks

While personal loans offer many advantages, borrowers should also understand potential risks.

Interest Costs

Borrowers pay interest over the life of the loan.

Late Payment Fees

Missing payments may result in additional charges.

Impact on Credit

Failure to repay responsibly can negatively affect credit profiles.

Borrowing Beyond Your Means

Taking on excessive debt can create financial stress.

Types of Personal Loans

Emergency Personal Loans

Designed for urgent financial situations requiring immediate access to funds.

Debt Consolidation Loans

Used to combine multiple debts into a single payment.

Medical Loans

Help cover healthcare-related expenses.

Wedding Loans

Provide financing for wedding-related costs.

Home Improvement Loans

Support renovation and property improvement projects.

Bad Credit Personal Loans

Offer financing options for borrowers with less-than-perfect credit histories.

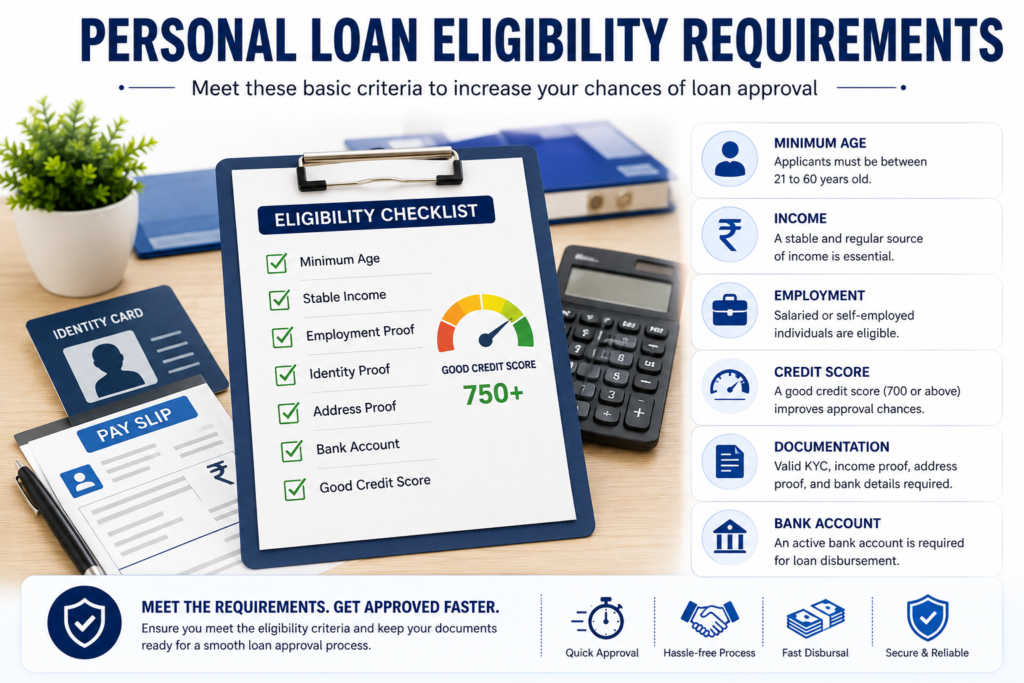

Eligibility Requirements

Although requirements vary among lenders, common criteria include:

- Minimum age requirement

- Proof of identity

- Stable income source

- Valid contact information

- Bank account details

- Satisfactory credit profile (where applicable)

Documents Required

Applicants may need to provide:

- Government-issued identification

- Proof of income

- Employment verification

- Bank statements

- Utility bills or address verification

Factors Affecting Approval

Credit History

A positive repayment history often improves approval chances.

Income Stability

Lenders prefer borrowers with reliable income sources.

Debt-to-Income Ratio

Lower debt levels generally strengthen applications.

Employment Status

Stable employment can positively influence lending decisions.

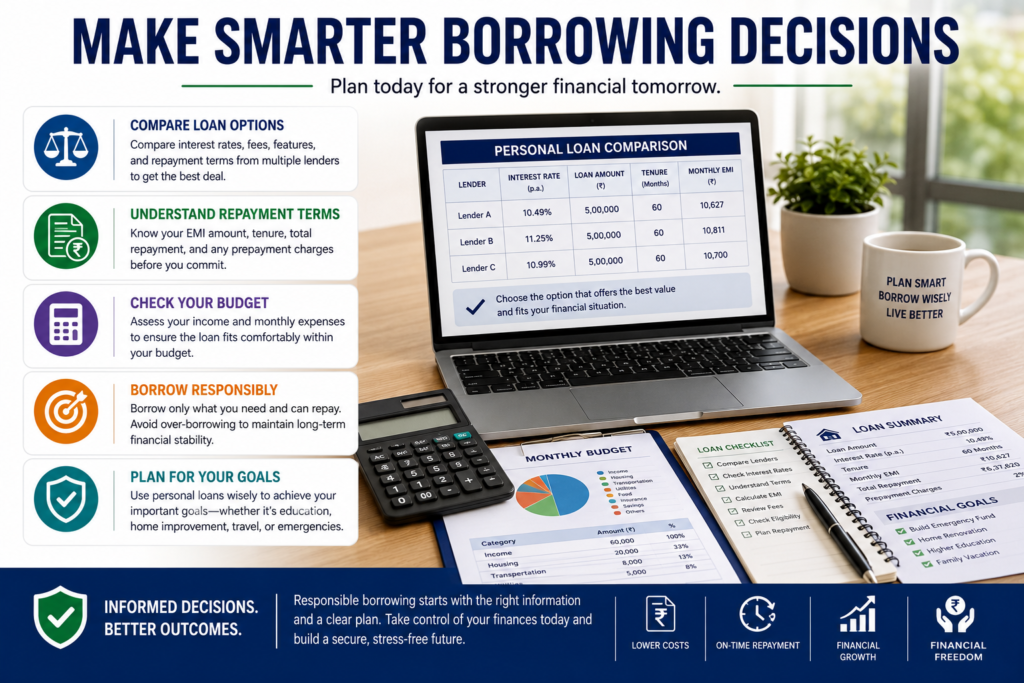

How to Improve Approval Chances

Review Your Credit Profile

Check for errors and address any inaccuracies.

Reduce Existing Debt

Pay down balances before applying.

Maintain Stable Employment

Consistency demonstrates financial reliability.

Borrow Only What You Need

Smaller loan requests may improve approval odds.

Compare Multiple Lenders

Evaluate different options before making a decision.

Responsible Borrowing Tips

- Borrow only when necessary.

- Create a realistic repayment budget.

- Understand all fees and charges.

- Avoid borrowing for unnecessary purchases.

- Make payments on time.

- Maintain an emergency savings fund.

Common Mistakes to Avoid

Applying for Too Many Loans

Multiple applications within a short period may affect approval outcomes.

Ignoring Loan Terms

Always read and understand all conditions.

Missing Payments

Late payments can lead to penalties and financial difficulties.

Borrowing More Than Needed

Excessive borrowing increases repayment obligations.

Frequently Asked Questions

What can a personal loan be used for?

Personal loans may be used for debt consolidation, home improvements, medical expenses, emergencies, education costs, and other legitimate financial needs.

Are personal loans secured or unsecured?

Many personal loans are unsecured, although secured options are also available.

How long does approval take?

Approval times vary depending on the lender and application requirements.

Can I repay a personal loan early?

Many lenders allow early repayment, although terms may vary.

Do personal loans affect credit scores?

Yes. Responsible repayment can support credit health, while missed payments may have negative effects.

Conclusion

Personal loans can be valuable financial tools when used responsibly. By understanding how they work, evaluating loan options carefully, and maintaining a realistic repayment plan, borrowers can make informed financial decisions that support their long-term goals.

Before applying, compare available options, review eligibility requirements, and ensure the loan aligns with your financial needs and repayment capabilities. Responsible borrowing is the foundation of long-term financial stability and success.