Introduction

Managing multiple debts can be overwhelming. Many individuals juggle credit card balances, personal loans, medical bills, and other financial obligations, each with different interest rates, payment schedules, and due dates. Keeping track of multiple payments can increase financial stress and make budgeting more difficult.

Debt consolidation loans are designed to simplify debt management by combining multiple debts into a single loan with one monthly payment. While debt consolidation may not eliminate debt entirely, it can help borrowers organize their finances and potentially improve their ability to manage repayment.

This comprehensive guide explains how debt consolidation loans work, their benefits, potential risks, eligibility requirements, and important factors to consider before applying.

What Is a Debt Consolidation Loan?

A debt consolidation loan is a type of financing used to combine multiple existing debts into a single loan. Instead of making several payments to different creditors each month, borrowers use the consolidation loan to pay off qualifying debts and then make one payment toward the new loan.

The primary goal of debt consolidation is to simplify repayment and improve financial organization.

Depending on individual circumstances and lender terms, consolidation may also help borrowers secure more manageable repayment structures.

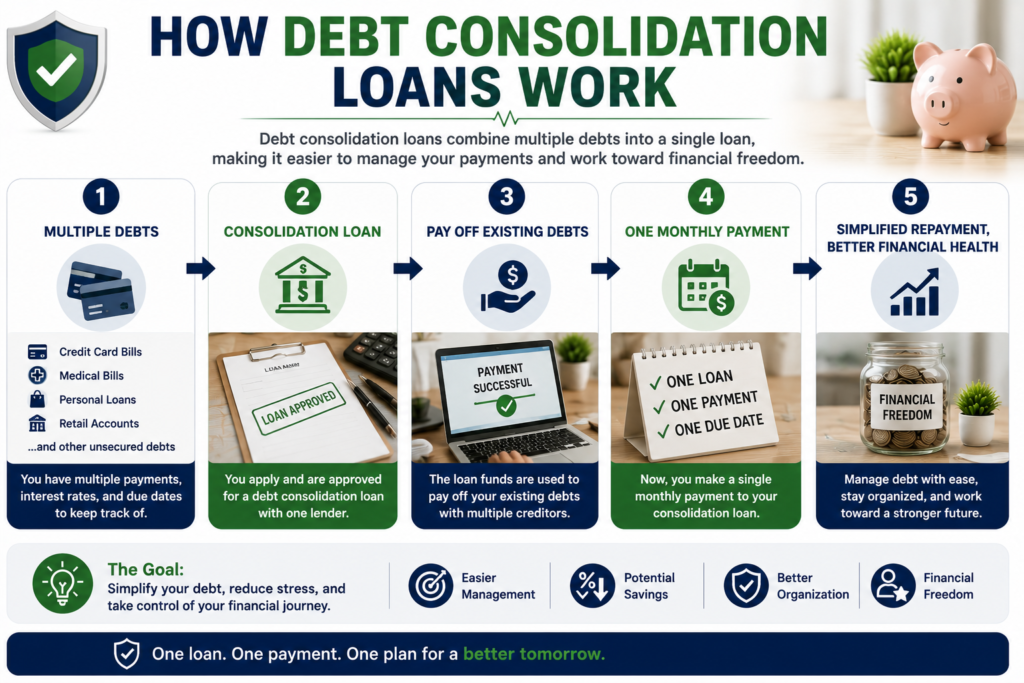

How Debt Consolidation Loans Work

The debt consolidation process generally follows several steps.

Assess Existing Debts

Borrowers review their current debts, balances, interest rates, and monthly payments.

Apply for a Consolidation Loan

Applicants provide personal, financial, and income information to a lender.

Loan Approval

If approved, the lender offers financing based on eligibility criteria.

Debt Repayment

The loan proceeds are used to pay off eligible existing debts.

Single Monthly Payment

The borrower repays the new consolidation loan through one monthly payment.

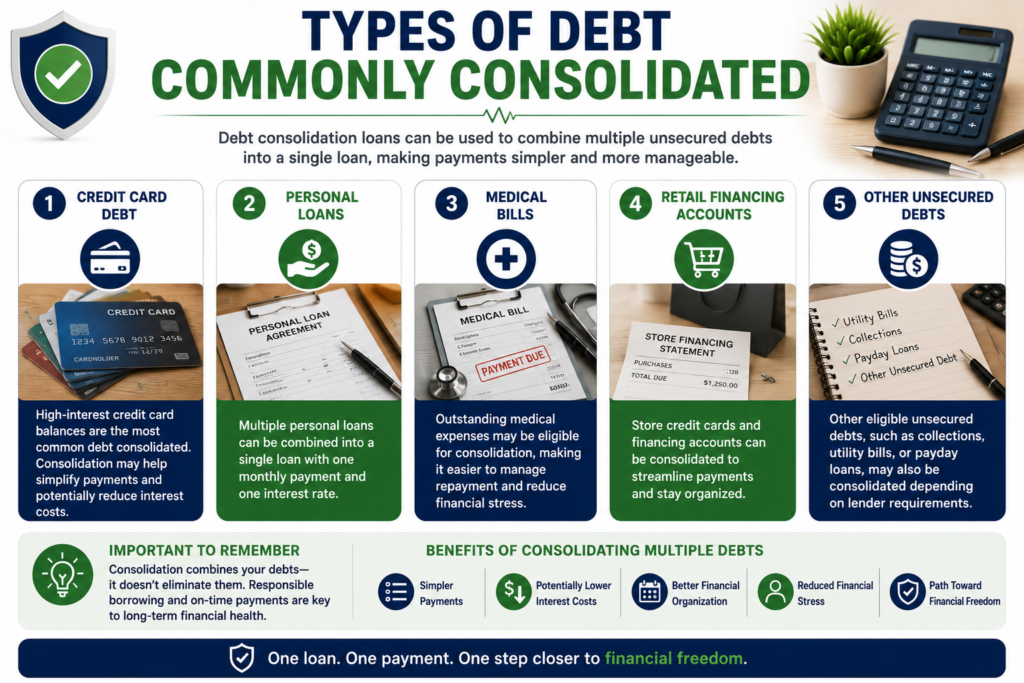

Types of Debt Commonly Consolidated

Credit Card Debt

High-interest credit card balances are among the most common debts consolidated.

Personal Loans

Multiple personal loans may be combined into one repayment plan.

Medical Bills

Healthcare-related expenses may sometimes be included in debt consolidation strategies.

Retail Financing Accounts

Store financing balances may be eligible depending on lender requirements.

Other Unsecured Debts

Certain unsecured financial obligations may qualify for consolidation.

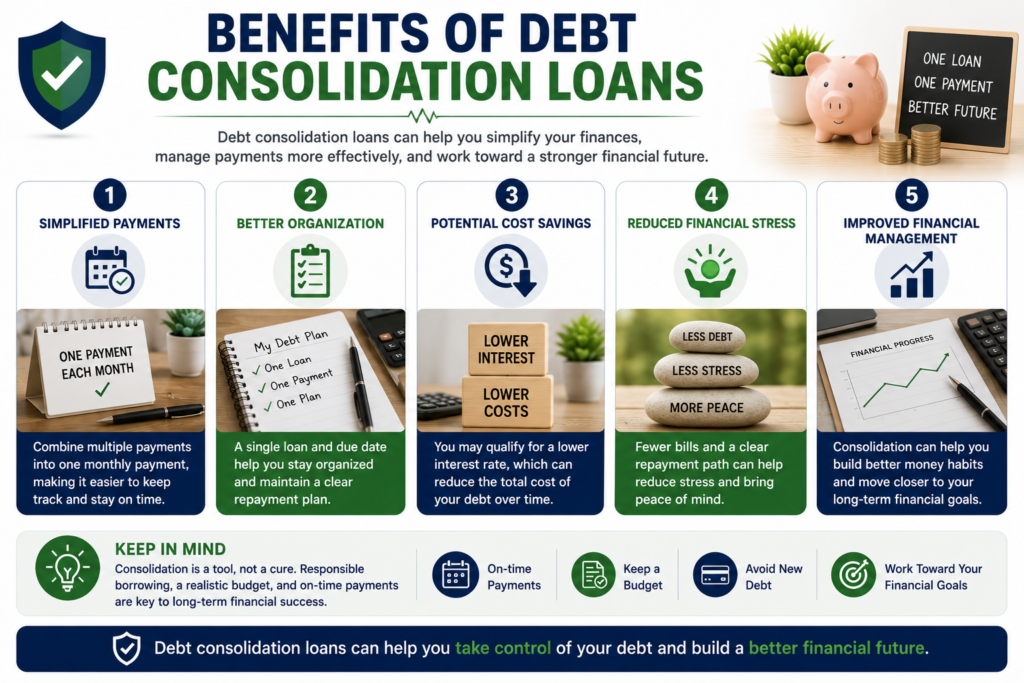

Benefits of Debt Consolidation Loans

Simplified Financial Management

One monthly payment is often easier to manage than multiple due dates.

Better Organization

Debt consolidation can help individuals gain a clearer picture of their financial obligations.

Potentially Lower Interest Costs

Depending on creditworthiness and lender terms, some borrowers may qualify for more favorable rates.

Improved Budgeting

A single payment may make monthly budgeting more predictable.

Reduced Financial Stress

Managing fewer payments can help reduce the stress associated with multiple debt obligations.

Potential Risks and Considerations

Not All Debt Is Eliminated

Debt consolidation reorganizes debt rather than eliminating it.

Interest Costs Still Apply

Borrowers remain responsible for repayment according to loan terms.

Fees and Charges

Some lenders may charge origination fees or other costs.

Risk of New Debt Accumulation

Continuing to use credit after consolidation may create additional financial challenges.

Longer Repayment Terms

Lower monthly payments may result in longer repayment periods.

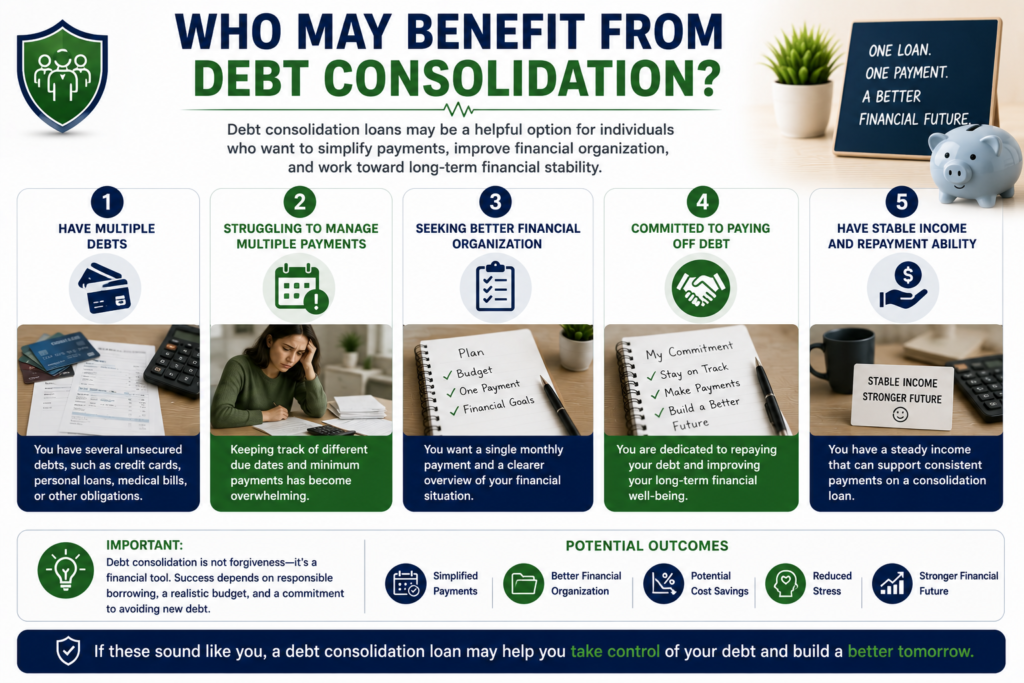

Who May Benefit from Debt Consolidation?

Debt consolidation may be appropriate for individuals who:

- Have multiple unsecured debts

- Struggle to manage several monthly payments

- Want a more organized repayment structure

- Are committed to reducing debt responsibly

- Have stable income to support repayment

Eligibility Requirements

Requirements vary by lender but often include:

Identity Verification

Government-issued identification may be required.

Income Verification

Proof of income helps demonstrate repayment ability.

Employment Information

Lenders may review employment stability.

Banking Information

Active banking details are often required.

Credit Assessment

Credit history may influence approval and loan terms.

Documents Commonly Required

Applicants may be asked to provide:

- Government-issued ID

- Proof of income

- Employment verification

- Bank statements

- Proof of address

- Existing debt information

Responsible Debt Consolidation Strategies

Create a Budget

Develop a realistic monthly budget that supports repayment goals.

Avoid New Debt

Limit unnecessary borrowing after consolidating existing obligations.

Make Payments on Time

Consistent payments can support long-term financial health.

Track Progress

Monitor balances and repayment milestones regularly.

Build Emergency Savings

Establishing an emergency fund can help reduce future borrowing needs.

Alternatives to Debt Consolidation Loans

Debt Management Plans

Professional debt management services may assist eligible individuals.

Balance Transfer Options

Some borrowers explore balance transfer opportunities for qualifying debts.

Direct Negotiation with Creditors

Certain creditors may offer repayment arrangements.

Emergency Savings

Savings can help reduce reliance on future borrowing.

Financial Counseling

Professional financial guidance may help individuals develop repayment strategies.

Frequently Asked Questions

What is a debt consolidation loan?

A debt consolidation loan combines multiple debts into a single loan with one monthly payment.

Does debt consolidation eliminate debt?

No. Debt consolidation reorganizes debt into a new repayment structure but does not eliminate the amount owed.

Can credit card debt be consolidated?

Many borrowers use consolidation loans to manage credit card balances, depending on lender requirements.

Is debt consolidation right for everyone?

Not necessarily. Individual financial situations vary, and borrowers should carefully evaluate all available options.

Should I compare multiple lenders?

Yes. Comparing lenders can help borrowers evaluate costs, repayment terms, and loan suitability.

Conclusion

Debt consolidation loans can provide a practical way to simplify debt repayment and improve financial organization. By combining multiple obligations into a single loan, borrowers may find it easier to manage payments, track progress, and work toward long-term financial stability.

However, successful debt consolidation requires responsible borrowing, disciplined budgeting, and a commitment to avoiding unnecessary debt accumulation. Understanding how consolidation works and carefully evaluating available options can help borrowers make informed financial decisions that support their long-term goals.