Introduction

Healthcare expenses can arise unexpectedly and place significant financial pressure on individuals and families. Whether facing an emergency medical procedure, surgery, dental treatment, fertility services, vision correction, or ongoing healthcare costs, many people seek financing options to help manage these expenses.

Medical loans are one financing solution that can help cover healthcare-related costs when immediate payment is not possible. Understanding how medical loans work, their benefits, potential risks, eligibility requirements, and alternative financing options can help borrowers make informed financial decisions during challenging times.

This comprehensive guide explores everything you need to know about medical loans, helping you understand when they may be appropriate and how to use them responsibly.

What Is a Medical Loan?

A medical loan is a type of personal loan designed to help individuals pay for healthcare-related expenses. These loans can be used for a wide variety of medical treatments and procedures, depending on the lender’s terms and conditions.

Medical loans typically provide a lump sum amount that borrowers repay through fixed monthly installments over an agreed period.

Unlike health insurance, which helps cover eligible healthcare costs based on policy terms, medical loans provide financing that must be repaid according to the loan agreement.

Common Uses for Medical Loans

Medical loans may be used for various healthcare-related expenses, including:

Emergency Medical Expenses

Unexpected medical emergencies can result in significant costs that require immediate attention.

Surgical Procedures

Medical loans may help finance necessary surgeries not fully covered by insurance.

Dental Treatments

Borrowers often use medical financing for major dental procedures such as implants, orthodontics, and restorative treatments.

Vision Care

Certain vision-related treatments and procedures may be financed through medical loans.

Fertility Treatments

Some individuals use financing options to help manage the costs associated with fertility-related healthcare services.

Specialist Care

Medical loans may assist with expenses related to specialist consultations and treatment plans.

Ongoing Healthcare Costs

Certain long-term healthcare expenses may create financial challenges that borrowers seek to manage through financing solutions.

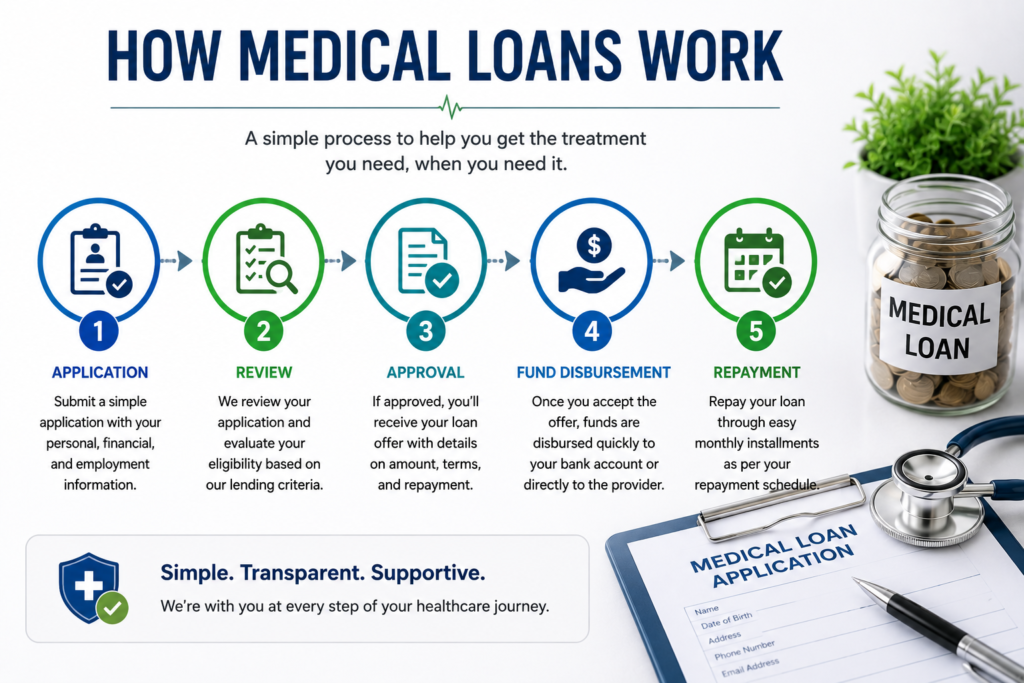

How Medical Loans Work

The process for obtaining a medical loan generally follows several steps.

Application

Borrowers submit an application with personal, financial, and income information.

Review Process

Lenders evaluate eligibility based on their lending criteria.

Approval Decision

Qualified applicants may receive approval for a specific loan amount.

Funding

Approved funds are typically disbursed according to the lender’s procedures.

Repayment

Borrowers repay the loan through scheduled monthly payments that include principal and interest.

Benefits of Medical Loans

Access to Timely Healthcare

Medical financing can help individuals obtain necessary treatment without extended delays.

Predictable Monthly Payments

Many medical loans provide fixed repayment schedules that simplify budgeting.

Flexible Loan Amounts

Borrowers may be able to finance a variety of healthcare expenses depending on lender policies.

No Need to Delay Important Procedures

Financing may allow patients to move forward with treatment plans when immediate funds are unavailable.

Potential Alternative to High-Interest Debt

Some borrowers prefer structured medical financing instead of relying on high-interest revolving debt.

Potential Risks and Considerations

While medical loans can be useful, borrowers should carefully consider the associated responsibilities.

Interest Costs

Borrowers typically pay interest on financed amounts.

Additional Fees

Some financing arrangements may include fees and charges.

Long-Term Financial Obligations

Monthly payments become part of the borrower’s ongoing financial commitments.

Borrowing More Than Necessary

Individuals should only finance amounts genuinely needed for healthcare expenses.

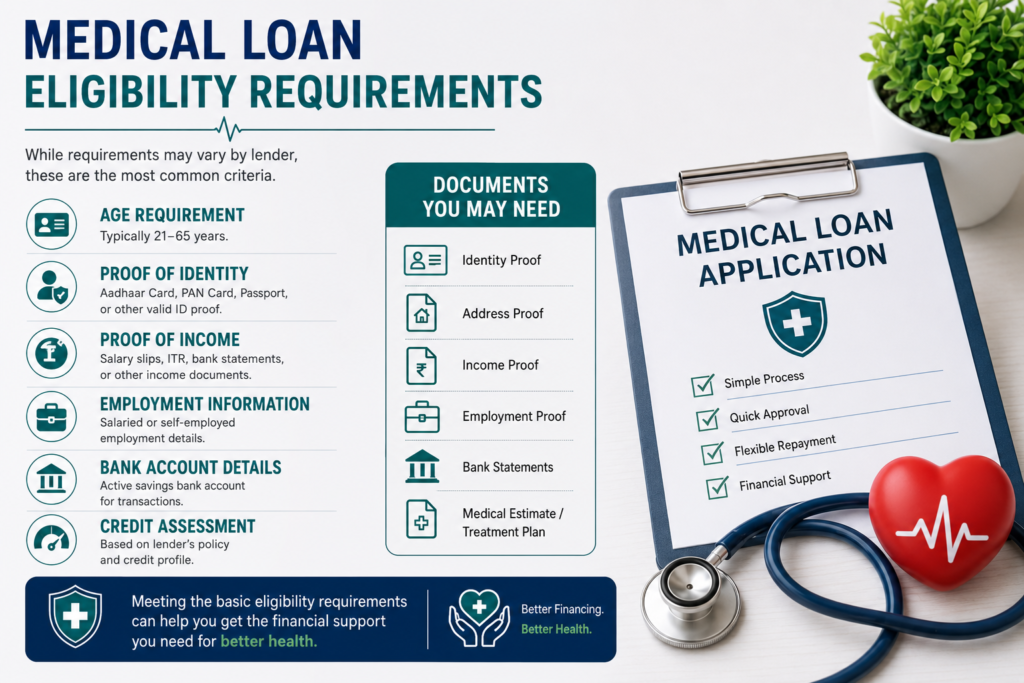

Eligibility Requirements

Requirements vary among lenders, but common factors include:

- Age requirements

- Proof of identity

- Income verification

- Employment information

- Bank account details

- Credit assessment (where applicable)

Meeting eligibility criteria does not guarantee approval, as lending decisions vary by provider.

Documents Commonly Required

Applicants may be asked to provide:

- Government-issued identification

- Proof of income

- Employment verification

- Bank statements

- Proof of address

- Healthcare-related documentation when required

Factors That Influence Approval

Income Stability

Reliable income demonstrates repayment capability.

Existing Financial Obligations

Lenders may evaluate current debt commitments.

Credit Profile

Past financial behavior may influence lending decisions.

Loan Amount Requested

The requested amount may impact eligibility assessments.

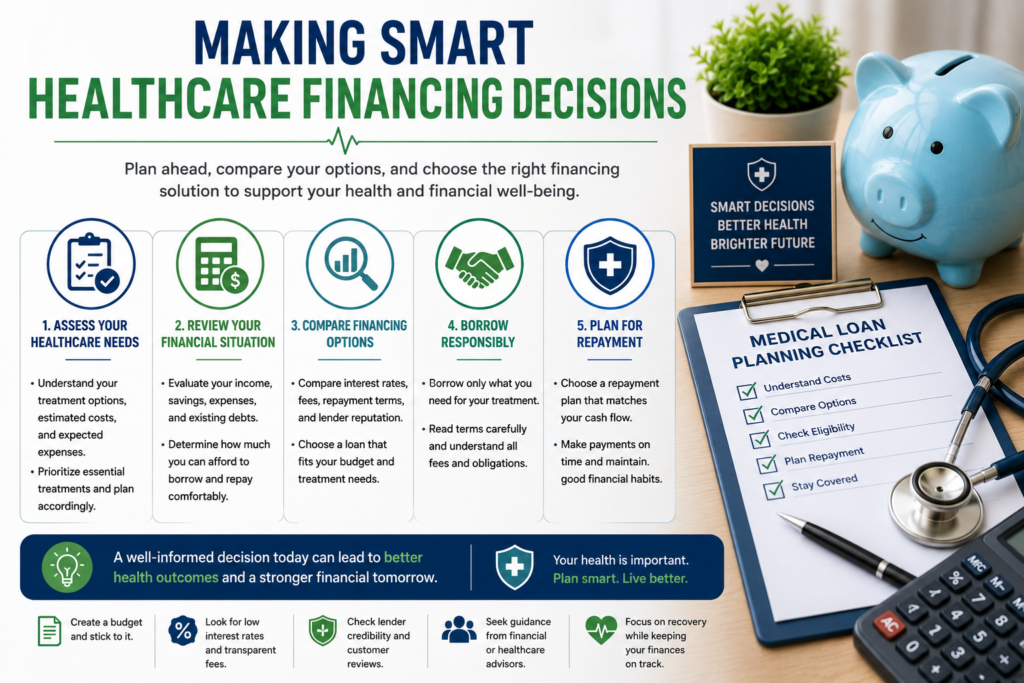

Responsible Borrowing Tips

Understand Total Costs

Review all interest charges, fees, and repayment obligations before accepting financing.

Compare Multiple Options

Evaluate several financing solutions before making a decision.

Borrow Only What You Need

Avoid financing unnecessary expenses.

Maintain a Repayment Plan

Create a realistic budget to support on-time payments.

Keep Emergency Savings

Continue building financial reserves whenever possible.

Alternatives to Medical Loans

Before applying for a medical loan, borrowers may also consider:

Health Insurance Benefits

Review policy coverage and available benefits.

Hospital Payment Plans

Many healthcare providers offer payment arrangements.

Health Savings Accounts

Eligible individuals may use healthcare savings accounts for qualifying expenses.

Family Assistance

Some individuals receive temporary support from family members.

Community Assistance Programs

Certain nonprofit organizations may provide financial assistance for eligible patients.

Frequently Asked Questions

What is a medical loan?

A medical loan is a financing option used to help cover healthcare-related expenses through structured monthly repayments.

Can medical loans be used for dental treatment?

Depending on lender policies, medical financing may be used for eligible dental procedures.

Are medical loans secured or unsecured?

Many medical loans are unsecured, although options vary by lender.

How long does repayment take?

Repayment periods vary based on lender terms and the amount financed.

Should I compare multiple lenders?

Yes. Comparing options helps borrowers evaluate costs, repayment terms, and overall suitability.

Conclusion

Medical loans can provide financial flexibility when healthcare expenses create unexpected challenges. However, borrowing should always be approached carefully and responsibly. Understanding loan terms, comparing financing options, evaluating repayment obligations, and considering alternatives can help borrowers make informed decisions that support both their health and financial well-being.

When used wisely, medical loans can serve as a practical tool for managing healthcare expenses while maintaining long-term financial stability.